Cigar Industry Trends & Legislation: Growth in the U.S.

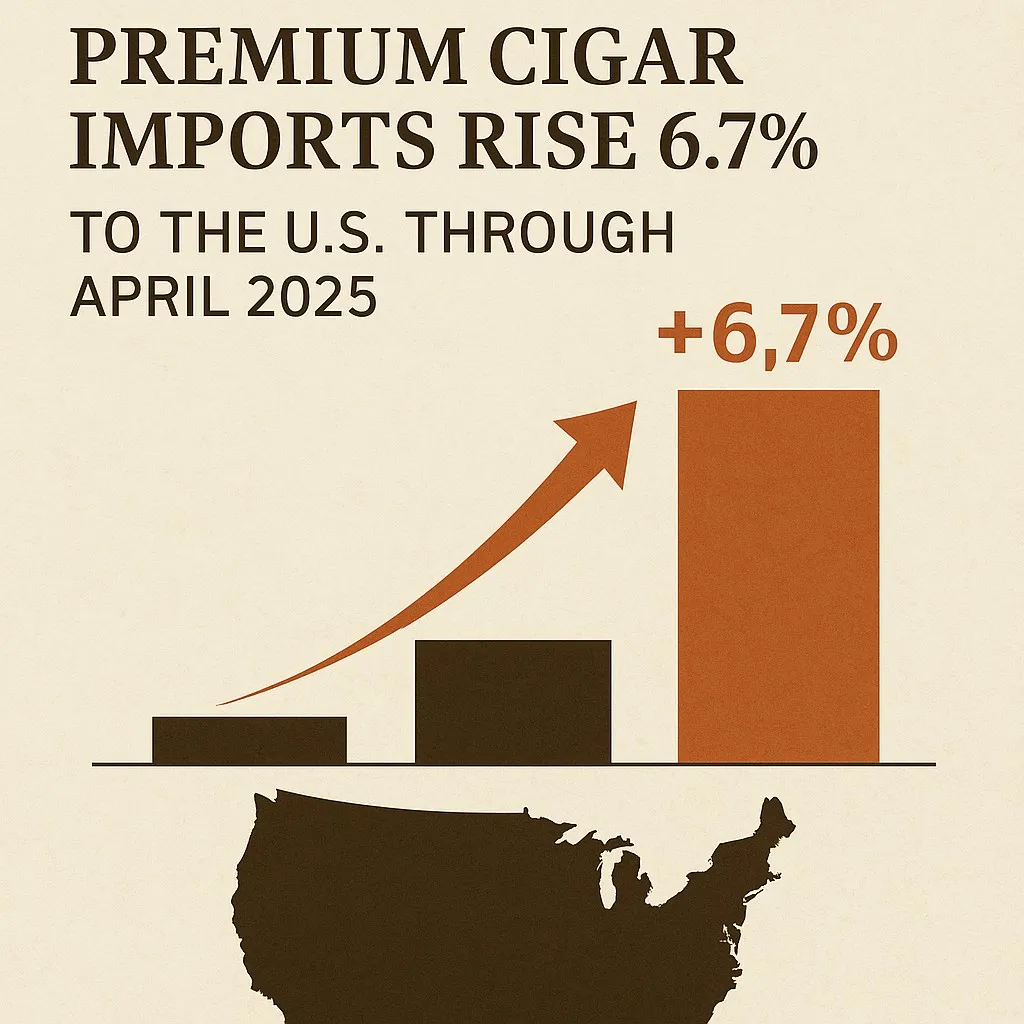

The US cigar industry posted 6.7% import growth through April 2025 — the strongest premium cigar performance in five years. What's driving it, where the growth is coming from, and which forces could derail it.

The premium cigar world is splitting in two. In the United States, the US cigar industry is having its strongest year since the pre-pandemic peak — handmade imports rose 6.7% through April 2025 compared to 2024, lounges are opening at the fastest rate in a decade, and younger demographics are entering the category in numbers nobody expected. Meanwhile in Europe, a sweeping new tobacco tax proposal threatens to cut the EU cigar market in half by 2028.

Two markets, two trajectories. The decisions made in 2026 on both sides of the Atlantic will reshape who smokes premium cigars, where the boutique brands grow, and which retailers survive the next decade.

US premium cigar imports: 6.7% growth through April 2025

The headline number comes from US Census Bureau trade data on handmade cigar imports — a clean leading indicator of premium cigar demand because virtually all US premium cigar consumption is imported (the domestic premium production is a rounding error). Through April 2025, year-over-year import growth hit 6.7%, well ahead of the ~2% the industry analyst consensus expected for the year.

For context: that’s the strongest performance since 2018-2019. The pandemic spike in 2020-2021 was real but artificial — people couldn’t go to lounges, so home consumption surged. The 2022-2024 correction took that air out. What’s happening now is a genuine demand expansion, not a base effect.

The 6.7% number understates the boutique-brand growth specifically. Mainstream brands (Padrón, Arturo Fuente, Davidoff) grew low single-digits. Boutique brands (the smaller artisanal producers in Nicaragua, Honduras, and increasingly Costa Rica) grew 15-25% depending on the segment. Premium is bifurcating into mass-luxury and true craft, and the craft side is where the heat is.

Four forces driving the growth

1. Luxury repositioning. Premium cigars are increasingly bought and discussed as luxury lifestyle objects rather than tobacco products. The audience overlaps with watch collecting, whiskey aging, and specialty coffee — categories where the buyer profile is willing to spend on experience and story, not just product. Brand marketing has followed: lookbooks, factory tours, founder profiles. The category looks more like fine wine than the 1990s cigar boom.

2. The lounge renaissance. Cigar lounges in the US are opening at the fastest rate since the late 1990s. States with permissive smoking laws (Florida, Texas, Pennsylvania, Connecticut) lead the count, but even restrictive markets like California and New York have seen new private-club-style lounges pass code via membership-only structures. The lounges drive boutique brand sales — once a smoker tries a Liga Privada or My Father in a lounge, they buy a box for home.

3. Post-pandemic supply stability. The 2020-2022 disruptions broke supply chains across the cigar industry — particularly cedar packaging from Honduras and aged wrapper leaf shipped from Nicaragua. Those chains have largely recovered. Retailers can stock consistently again, and consumers who left the category during the disruption are returning.

4. Generational entry. This is the surprise of 2025. Millennials and Gen Z buyers are entering the premium cigar market at noticeably higher rates than analysts expected. The driver: curated experiences. Cigars paired with whiskey tastings, social media storytelling around cigar lounges, and the broader rise of “slow consumption” as a counter to digital overload. The under-35 buyer profile skews more toward boutique brands and accessories — which is reshaping retailer assortments. Our eight cigar lifestyle pieces worth owning roundup leans into exactly this audience: aficionados who care about the gear as much as the cigar.

Where the imports come from

Nicaragua continues to dominate as the largest single source of US premium cigar imports, with Padrón, My Father, Plasencia, and a long tail of boutique producers driving the bulk. The Dominican Republic is the steady #2 — anchored by Arturo Fuente, Davidoff’s Dominican line, and the General Cigar portfolio. Honduras is #3 and growing fastest among the top three.

The fast-rising sources to watch: Costa Rica (boutique producers leveraging Costa Rican-grown wrapper varieties), Mexico (San Andrés wrapper specifically, increasingly used by Nicaraguan-blended cigars), and small-batch Ecuadorian Connecticut shade wrappers that have replaced traditional Connecticut for much of the industry. The Cuban vs Dominican wrapper landscape we covered separately remains the foundational divide, but the supply geography is more layered than that in 2025.

What could derail the growth

The 6.7% trajectory isn’t guaranteed to continue. Three risks worth tracking:

- FDA premium cigar regulation. The 2016 ruling subjecting premium cigars to FDA tobacco oversight has been litigated for nearly a decade. A 2023 court ruling exempted premium cigars from many of the original requirements, but the FDA has appealed and the case isn’t settled. A reversal would impose substantial compliance costs on small importers.

- The EU tobacco tax directive ripple effect. If the proposed 1,100% EU cigar tax floor passes in 2026-2027, European producers and distributors will reorient toward US and Asian markets, which would pressure US import prices upward and reshape brand availability.

- Cuban embargo changes. Either direction. If the embargo loosens, Cuban brands flood the US market and disrupt the existing Nicaraguan/Dominican dominance. If it tightens further (more enforcement against personal-use cross-border purchases), Cuban demand stays where it is. Both scenarios change brand allocations.

What this means for buyers in 2026

For US-based aficionados, the implication of the growth data is simple: boutique brand availability will be tight on releases. The 15-25% boutique segment growth is outstripping production expansion. Limited Editions and small-batch releases that used to sit on shelves for a month now sell through in days. Our coverage of Edición Limitada releases like Montecristo Elba and Punch Princesas reflects this dynamic — those are products you decide on within hours of release, not weeks.

For retailers, the strongest opportunity continues to be lounge-attached models: the lounge drives discovery, the attached retail captures the box purchase. Standalone retail without an experiential component is losing share.

For investors and brand operators in adjacent categories — humidors, lighters, cutters, lifestyle apparel — the rising tide is real. Our best cigar cutters of 2026 roundup and best cigar lighters of 2026 roundup reflect demand growth on the accessories side that mirrors the premium cigar import growth almost one-to-one.

For source data on US trade and consumption trends, the Cigar Association of America publishes quarterly market reports that are the canonical reference.

The US cigar industry’s 2025 growth is real, broad-based, and structurally durable. The question for 2026-2028 isn’t whether the category continues to grow but where the growth is captured — in mass-luxury brands, in boutique craft, or in entirely new categories the lounges haven’t surfaced yet. Stay tuned to the Sunday newsletter for the next round of import data when Q2 numbers land.

Filed under

Latest News